Secured vs. unsecured loans

Secured vs. Unsecured Loans: What’s the Difference for Indian Borrowers?

Secured loans and unsecured loans form the backbone of India’s growing retail credit market, offering individuals and businesses access to funds for a wide range of financial needs. As credit demand continues to rise across urban, Tier-2, and Tier-3 regions, many borrowers now rely on loans for housing, education, healthcare, small-business expansion, and emergencies.

At the same time, the Reserve Bank of India has tightened norms around unsecured consumer credit, prompting banks and NBFCs to evaluate risk more carefully before approving new loans. This makes it even more important for borrowers to understand how these two loan types differ in terms of interest rates, eligibility, risk, and repayment structure.

Whether someone is a salaried professional, self-employed entrepreneur, or first-time borrower, choosing the right loan product can impact long-term financial stability. A clear understanding ensures borrowing remains a tool for progress rather than future stress.

How Secured and Unsecured Loans Work

Both secured and unsecured loans allow a borrower to access funds, repay them over time, and pay interest according to a pre-agreed repayment schedule. In both cases, lenders evaluate income, existing obligations, and credit history before sanctioning a loan.

The key difference is risk sharing:

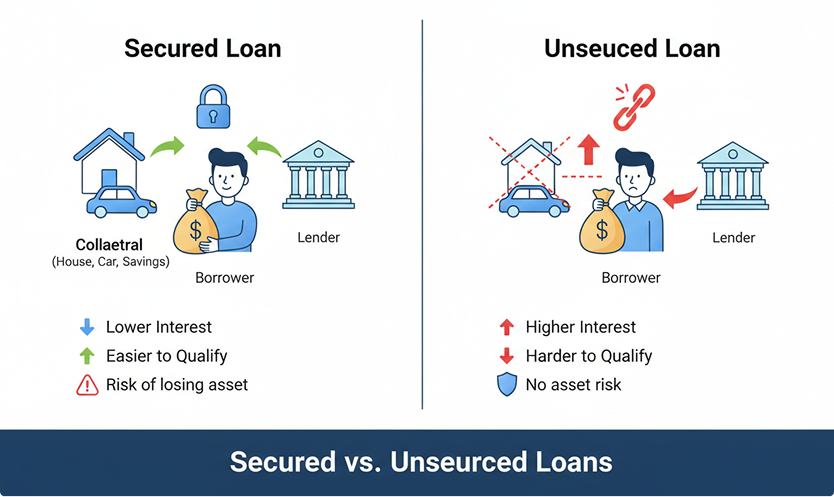

- In a secured loan, the borrower pledges an asset such as property, a vehicle, gold, or a fixed deposit as collateral. If the loan is not repaid, the lender can enforce its rights over that asset.

- In an unsecured loan, no collateral is pledged. The lender relies primarily on the borrower’s repayment capacity and credit profile. This higher risk is reflected in tighter eligibility and generally higher interest rates.

Key Takeaways

- Secured loans are backed by collateral like a home, gold, or vehicle, which allows lower interest rates, higher loan amounts, and longer tenures.

- Unsecured loans do not require collateral, making them faster and easier to access, but they come with higher interest rates and stricter loan eligibility rules.

- Lenders evaluate income, credit score, and repayment behaviour for both loan types, as per RBI norms, to safeguard against rising delinquency in the retail credit market.

- Borrowers should compare total cost of credit (interest + fees), EMI affordability, and loan purpose before choosing secured vs unsecured financing.

What Is a Secured Loan?

A secured loan is a credit facility backed by collateral. The collateral’s value typically covers all or most of the loan amount, which reduces the lender’s potential loss in case of default.

Common examples in India include:

- Home loans and loans against property

- Auto and two-wheeler loans

- Gold loans

- Loans against fixed deposits, LIC policies, or market securities

- Secured business loans backed by property or equipment

These products are widely used for large purchases and long-term needs where borrowers are comfortable pledging an asset in exchange for better pricing.

Pros and Cons of Secured Loans

Pros

Lower interest rates

Because the lender can recover dues from collateral, secured loans are usually priced lower than comparable unsecured loans. Home loans and gold loans remain among the cheapest retail credit products.

Higher loan amounts

The sanctioned amount can be significantly higher, particularly for home loans, loans against property, and secured business loans, since it is linked to collateral value rather than only income.

Longer tenures

Secured loans often offer long repayment periods, for example up to 20-30 years for housing loans, which helps keep monthly EMIs relatively manageable.

Cons

Risk of asset loss

If the borrower defaults and restructuring or settlement is not possible, the lender can enforce security and sell the asset. This may mean losing a home, business property, or family gold.

More documentation and processing time

Property title checks, valuation reports, legal scrutiny, and other due diligence steps make secured loans slower and more complex to process than a typical personal loan.

Asset remains locked

While a property or gold is pledged, it cannot easily be used as security for another loan. Prepayment or closure is often required before it is released.

What Is an Unsecured Loan?

An unsecured loan is a credit facility that does not require any collateral. Approval depends on factors such as income, occupation, credit score, repayment track record, and existing leverage.

Common unsecured products in India include:

- Personal loans from banks and NBFCs

- Credit card outstanding and credit card loans

- Consumer durable loans and some education loans

- Unsecured working capital or term loans for small businesses and professionals

These products are widely used for medical expenses, weddings, travel, home interiors, small business needs, and debt consolidation.

Pros and Cons of Unsecured Loans

Pros

No collateral required

Borrowers are not required to pledge property, gold, or deposits. This is useful for young earners, tenants, or borrowers who do not wish to risk assets.

Faster approval and disbursal

With digital KYC, income checks, and bureau pulls, unsecured personal loans and credit card loans can be sanctioned quickly, sometimes within hours, especially from existing banking relationships or fintech NBFCs.

Flexible end use

Except for specific restrictions (for example, speculative activity), unsecured personal loans usually allow broad, multipurpose usage.

Cons

Higher interest rates

Lenders price in higher credit risk, so unsecured loans generally carry higher interest rates than secured loans of similar tenure and profile.

Lower loan amounts and shorter tenures

Since there is no collateral, lenders limit ticket size and tenure. Large long-term requirements are therefore harder to meet with unsecured products alone.

Stricter eligibility and more sensitive to stress

Lenders closely evaluate credit scores, FOIR (fixed obligations to income ratio), and repayment behaviour. Recent data shows higher GNPA ratios on unsecured retail loans compared with the overall retail book, which makes lenders even more selective.

How to Choose Between Secured and Unsecured Loans

The right choice depends on purpose, amount, risk appetite, and financial position.

Secured loans may be more appropriate when:

- The borrower is purchasing or constructing a home, commercial property, or vehicle.

- A business requires a large loan for expansion or equipment, and property or machinery is available to pledge.

- The borrower wants to consolidate expensive debt using a lower-cost loan against property, gold, or deposits.

Unsecured loans may be more appropriate when:

- The need is short to medium term, for example a medical emergency, relocation, or wedding.

- The required amount is relatively small and speed of disbursal is important.

- The borrower does not own collateral or does not want to risk an asset, but has strong income and a healthy credit profile.

Irrespective of the loan type, borrowers should look beyond the headline interest rate and compare:

- Total cost of credit, including processing fees, insurance, and prepayment charges.

- EMI burden as a percentage of net monthly income.

- Impact on credit score in case of missed or delayed EMIs.

What Recent Trends Indicate

Regulatory and market developments in India over the last two years (2023-2025) have a direct bearing on the secured versus unsecured choice:

- The Reserve Bank of India increased risk weights on unsecured consumer credit and credit card receivables to slow aggressive growth in this segment and strengthen bank and NBFC capital buffers.

- Official data shows that the gross NPA ratio in unsecured retail loans is higher than the overall retail GNPA, indicating relatively greater stress in this category.

- Rating agencies expect credit costs to rise in unsecured loan portfolios, while secured segments such as housing finance remain comparatively stable.

For borrowers, this typically translates into:

- Tighter underwriting and more conservative limits on unsecured loans.

- Continued preference by lenders for secured assets such as home loans, vehicle loans, and loans against property or gold.

- Greater emphasis on bureau scores, past payment behaviour, and overall leverage when pricing and approving any new credit.

The Bottom Line

Secured and unsecured loans serve different needs in India’s evolving credit landscape. Secured loans provide access to larger amounts at relatively lower interest rates, but require an asset pledge and carry the risk of collateral loss. Unsecured loans offer speed and flexibility without collateral, but at higher cost and with stricter eligibility conditions.

With regulators closely watching unsecured lending and lenders sharpening their risk models, borrowers should assess loan purpose, repayment capacity, available collateral, and risk tolerance before choosing a product. A carefully selected mix of secured and unsecured credit, used sparingly and repaid on time, can support financial goals without undermining long-term financial health.

FAQs

Which is better, secured or unsecured loans?

Neither secured nor unsecured loans are “better” for everyone. Secured loans usually offer lower interest rates and higher amounts but require collateral and carry risk of asset loss. Unsecured loans are faster and do not need security, but cost more and have stricter eligibility. The better option depends on loan purpose, urgency, risk tolerance, and repayment capacity.

What is a secured loan and unsecured loan example?

A secured loan is backed by collateral. Common Indian examples include home loans, auto loans, gold loans, and loans against property or fixed deposits. An unsecured loan is given without collateral; examples include personal loans, credit card loans, and some small business or consumer durable loans. The key difference is whether an asset is pledged as security.

What are the disadvantages of a secured loan?

The main disadvantage of a secured loan is the risk of losing the pledged asset, such as a home, gold, or property, if EMIs are not repaid. Secured loans also involve more paperwork, legal checks, and valuation, so processing can be slower. In addition, the asset remains tied up as collateral and cannot be easily used for other borrowing.

Do unsecured loans hurt credit?

Unsecured loans do not automatically hurt credit. When EMIs are paid on time, they can actually help build a stronger credit history. Problems arise if EMIs are delayed, missed, or if multiple unsecured loans and credit cards push overall debt too high. In such cases, credit scores can fall and future borrowing may become more difficult and expensive.