How to choose the best lender for your loan

How to Choose the Best Lender for Loan in India

Choosing the right lender is just as important as choosing the right loan. Whether applying for a home loan, personal loan, auto loan or business loan, the lender you pick can influence your total borrowing cost, approval speed, overall experience and long-term financial stability. Digital lending is rapidly expanding and RBI regulations are tightening, borrowers must be more careful and informed than ever before.

Two loans with the same interest rate can still cost very different amounts if the lending terms, hidden charges and service quality vary. A trusted lender will not only offer competitive pricing but also ensure transparent communication, reliable support and secure technology to protect customer data.

This guide explains how to evaluate lenders in India, what criteria really matter and how to ensure that the loan you choose remains affordable and stress-free throughout its tenure.

Why Choosing the Right Lender Matters

A lender has a direct influence on:

- Interest rates and EMI affordability

- Loan approval chances

- Documentation and verification requirements

- Prepayment freedom and additional charges

- Customer service quality

- Data security and grievance handling

The wrong lender can cause unnecessary stress due to:

- Frequent hidden fees

- Penal charges for minor delays

- Complicated prepayment rules

- Aggressive recovery practices

- App or system failures during payment

A loan is a long-term commitment. Selecting a trustworthy lender helps maintain financial peace of mind.

Key Takeaways

- The best lender for loans is the one that offers transparent pricing, quick approvals, and customer-friendly service, not just the lowest headline interest rate.

- Always compare lenders based on the actual cost of the loan in India, processing fees, prepayment and foreclosure charges, and hidden loan costs to know the true expense.

- Check loan eligibility criteria, especially CIBIL score requirement, documentation flexibility, and whether the lender supports both salaried and self-employed profiles.

- Choose a loan lender in India that follows RBI guidelines for loans, ensures strong data protection, and provides reliable grievance support for a safe borrowing experience.

Types of Lenders in India

Borrowers today have multiple lending options:

| Lender Category | Characteristics | Ideal For |

|---|---|---|

| Public Sector Banks | Lowest interest rates but slower process | Home loans, secured loans |

| Private Banks | Faster, technology-enabled services | Higher-income and salaried borrowers |

| NBFCs | Flexible credit policies | Borrowers with lower scores or freelancers |

| Small Finance Banks | Support local and semi-urban borrowers | Small-ticket and micro loans |

| Digital-Only Lenders | Convenient mobile app approvals | Quick emergency and personal loans |

| Cooperative Banks | Community-based banking | Small business and rural borrowers |

Each type has pros and cons. The right choice depends on borrower profile and urgency of funds.

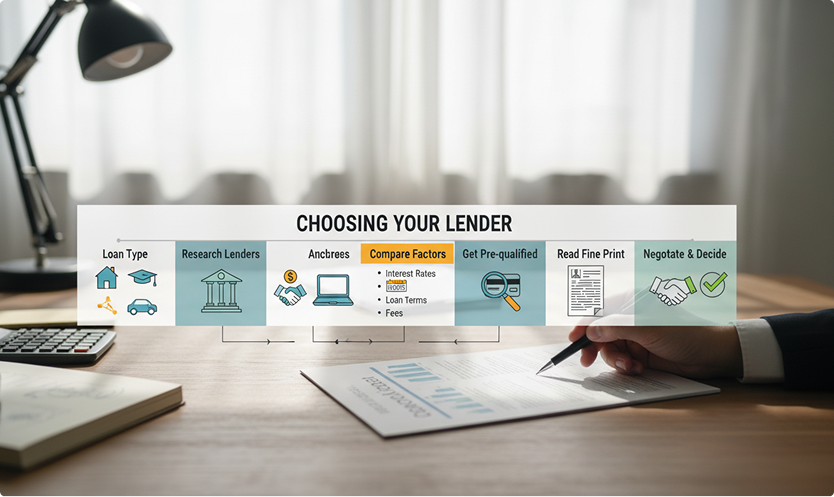

Key Factors to Compare Before Choosing a Lender

A smart evaluation includes more than just the interest rate.

A. Total Loan Cost

Compare:

- Interest rate (fixed or floating)

- Processing fee

- Prepayment or foreclosure charges

- Insurance premiums

- Annual maintenance charges

- GST on applicable fees

Always compare the actual cost of the loan, which shows how expensive the loan really is after adding interest and all charges.

B. CIBIL Score Requirements

A strong score unlocks:

- Lower pricing

- Higher loan amounts

- Faster approvals

Some lenders specialize in supporting borrowers with lower score profiles but charge more.

C. Loan Eligibility and Documentation

Check flexibility for:

- Self-employed borrowers

- Freelancers and gig workers

- Tier 2 and 3 city applicants

- First-time borrowers

D. Customer Experience and Support

Reliable service protects you from disruptions like:

- Auto-debit failures

- Incorrect EMI deductions

- Delayed NOC issuance

Review user ratings, app performance and grievance resolution efficiency.

E. Turnaround Time (TAT)

Digital lenders may offer:

- Instant approval

- Same-day disbursement

Banks may take longer due to risk checks but offer lower pricing.

F. Transparency and Communication

Trusted lenders provide:

- Clear Key Facts Statement

- Detailed sanction letter

- Written confirmation of every fee

- Pre-closure rules without ambiguity

G. Prepayment Flexibility

A good lender allows:

- Part-payment anytime after lock-in

- Zero or low foreclosure fees

- Choice to reduce EMI or tenure

H. Security and Data Protection

Verify whether the platform follows:

- RBI digital lending compliance

- Strong encryption

- Secure KYC processes

This prevents fraud and misuse of personal data.

How RBI Regulations Protect Borrowers

RBI has introduced strong rules in recent years to make lending fair and secure.

Borrowers now have:

- Key Facts Statement for full cost transparency

- Digital loan agreements with audit trails

- No automatic credit without explicit consent

- Restrictions on recovery methods and timing

- Mandatory grievance redressal setup

Understanding these rights helps borrowers avoid exploitation.

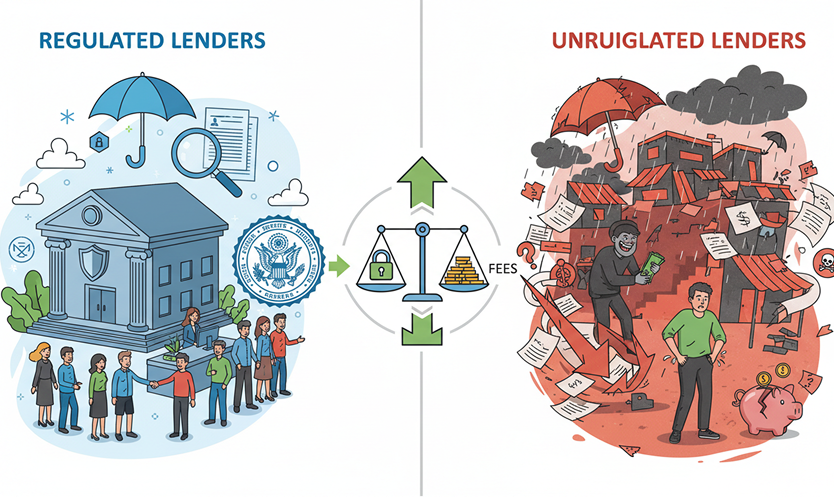

Digital Lending: Benefits and Red Flags

Digital lenders are reshaping India’s credit landscape.

Benefits

- Instant onboarding

- Minimal paperwork

- Easy tracking via mobile apps

- Quick disbursements for emergencies

Red Flags

Be cautious if a lender:

- Does not disclose full charges upfront

- Offers loans without credit checks

- Uses aggressive recovery techniques

- Requests unnecessary personal permissions in app

- Cannot be traced to a regulated entity

Borrow only from platforms linked to a bank or RBI-regulated NBFC.

Checklist to Select the Best Lender for Your Needs

| Evaluation Point | Why It Matters |

|---|---|

| Actual cost of the loan comparison | Identifies the truly cheapest loan |

| Prepayment rules | Helps reduce cost early |

| Customer ratings | Indicates trust and service quality |

| Flexibility in income proof | Supports non-salaried borrowers |

| Mobile app reliability | Ensures smooth repayments |

| Compliance with RBI norms | Ensures ethical business practice |

| Grievance mechanisms | Faster resolution of support issues |

Borrowers should shortlist 3 to 5 lenders and conduct a clear side-by-side comparison.

Common Mistakes to Avoid While Taking Loans

- Choosing based only on lowest advertised interest rate

- Ignoring penalty charges or insurance costs

- Not checking prepayment restrictions

- Applying to too many lenders at once

- Borrowing more than repayment capacity

- Not verifying lender’s regulatory status

- Relying only on approval speed

Avoiding these mistakes protects financial health in the long term.

The Bottom Line

Choosing the best lender is not about finding the first lender who says yes. It is about selecting a partner that supports your financial journey. A responsible lender provides fair pricing, transparent communication, reliable platforms and secure services.

To make the right choice:

- Compare total loan cost instead of just interest rate.

- Validate lender credibility and regulatory compliance.

- Ensure repayment terms are flexible and affordable.

- Review customer experience and digital trustworthiness.

A well-chosen lender not only helps get the loan approved but ensures peace of mind throughout the loan’s lifetime.

FAQs

How to decide which lender to go with?

The best way to decide is by comparing the total cost of borrowing, not just the interest rate. Review the actual cost of the loan, processing fees, prepayment rules, customer service quality, digital platform reliability, and transparency in terms. Make sure the lender is regulated by RBI and has a strong track record in grievance handling and borrower support.

How to choose a personal loan lender?

Choose a personal loan lender who offers competitive pricing, fast approvals, and clear terms without complicated hidden charges. Check their reputation, flexibility for documentation, and whether they consider your financial profile fairly. Reviewing customer reviews and service ratings can help determine if repayment and communication will be smooth throughout the loan tenure.

Can I get a 0% interest loan?

Zero percent interest loans are rare and usually available only on short-term consumer durable purchases like electronics or appliances. These offers often include processing fees, GST, or built-in vendor discounts. For cash personal loans or home loans, fully 0% interest is not offered in regulated lending as per RBI guidelines.

Who is the best loan lender in India?

There is no single best loan lender in India for everyone. The right lender depends on factors such as loan purpose, credit profile, interest rates, repayment terms, and urgency. Banks, reputed NBFCs, and digital platforms with RBI-regulated lending partners are generally considered reliable. Comparing transparency, costs, and service quality is essential before choosing a lender.

Common Hidden Charges in Loans

Processing Fees and GST

Processing fees are among the most common upfront charges. These are typically:

- A percentage of the loan amount (for example, 1-3% for many personal loans)

- Deducted from the sanction at disbursement, so the borrower receives less than the approved amount

On top of this fee, 18% GST is charged on the processing amount.

For example, on a Rs 5 lakh personal loan with a 3% processing fee:

- Processing fee = Rs.15,000

- GST @18% on fee = Rs.2,700

- Net credit to the borrower = Rs 4,82,300

The EMIs, however, are calculated on the full Rs 5 lakh principal, not the net credit.

Documentation, Legal and Valuation Charges

For home loans and loans against property, additional charges often include:

- Legal scrutiny fees for verifying title documents

- Valuation fees for property assessment

- Stamp duty and registration charges (where applicable)

These may be charged on an actual basis and must form part of the Actual cost of borrowing and be disclosed in the KFS if recovered by the lender.

Prepayment, Foreclosure and Part-Prepayment Charges

Depending on the loan type and nature of the interest rate:

- Floating-rate home loans to individuals: No prepayment/foreclosure penalties permitted.

- Other floating-rate loans to individuals: RBI directions in 2025 further limit prepayment charges, with full effect from January 2026.

- Fixed-rate loans and some NBFC products: Prepayment and foreclosure charges may still apply, especially in the first few years of the loan.

Borrowers should check:

- Whether prepayment is allowed partially or fully

- Whether there is a lock-in period (e.g. no prepayment for 12-24 months)

- The percentage charged on the outstanding amount (for example, 2-5%)

- Whether GST is applied on the prepayment fee (commonly at 18%)

Penal Charges and Late Payment Fees

When an EMI is delayed or terms are violated, lenders levy penal charges. After RBI’s 2023 circular:

- Penal charges cannot be simply added as extra interest; they must be shown separately.

- No compounding of penal charges is allowed.

However, these charges can still be substantial in practice, often expressed as:

- A fixed amount per month of default, or

- A percentage per annum on the overdue amount (for example, 24% p.a., charged as a monthly penalty)

Penal charges also generally attract GST.

EMI Bounce / Mandate Failure Charges

If an EMI is unpaid due to insufficient balance or technical failure, lenders may charge:

- Cheque bounce charges

- ECS/NACH/mandate failure charges

- Additional penal charges on overdue EMIs

These charges can range from a few hundred to over a thousand rupees per bounce in many retail products.

Repeated bounces not only increase costs but also negatively affect the credit profile and CIBIL score.

Conversion, Restructuring and Rate-Reset Fees

Many lenders charge fees for:

- Interest rate conversion (for example, moving from fixed to floating)

- Spread reduction (reducing the margin over benchmark for an existing home loan)

- Tenure changes or restructuring

These are sometimes marketed as “conversion offers” or “rate negotiation options” but are effectively chargeable services. They must form part of the loan’s overall cost disclosure when availed.

Insurance Bundled with Loans

It is common for lenders or partners to bundle:

- Credit life insurance

- Health or accident cover

- Property insurance (for secured loans)

When the lender recovers premium amounts, these must be part of Actual cost of borrowing and KFS, and borrowers are entitled to:

- Know whether insurance is optional or mandatory

- See separate documentation and receipts for premiums paid

Borrowers should confirm whether alternate policies are allowed and avoid feeling compelled into products that do not serve their needs.

Statement, Account Maintenance and Other Administrative Fees

Additional charges may include:

- Duplicate statement/interest certificate charges

- Loan account maintenance fees

- Re-issuance of amortisation schedules

- Copy of documents charges

Individually, these may appear small, but repeated usage can add up over the tenure.

How to Spot Hidden Charges Before Taking a Loan

To avoid unpleasant surprises:

- Read the KFS carefully

- Confirm Actual cost of borrowing, including all fees.

- Check whether any “other charges” are mentioned generically, ask for specifics.

- Request and review the Schedule of Charges: Processing fee, bounce charges, penal charges, statement fees, conversion fees etc.

- Examine the sanction letter and loan agreement: Look for clauses on prepayment, foreclosure, part-payment rules and lock-in periods.

- Ask for a “net disbursal illustration”: Approved amount vs. amount credited after all upfront deductions.

- Clarify tax treatment: Confirm where 18% GST is applicable and estimate the total impact.

All these documents should be provided in a language and format that borrowers can understand, as emphasised by RBI’s guidelines on KFS and transparency.

Checklist Before Signing a Loan Agreement

Before signing:

- Confirm the exact processing fee and GST impact

- Check whether any non-refundable upfront fees apply

- Understand prepayment and foreclosure rules clearly

- Note all penal charges, bounce fees and administrative charges

- Clarify if insurance is optional and whether alternative insurers are allowed

- Ensure all charges match what is disclosed in the KFS and sanction letter

- Retain copies of all signed documents, acknowledgements and receipts

If any fee appears at a later stage that was not mentioned in the KFS or sanction letter, borrowers can challenge it under the RBI’s fair lending and disclosure norms.

The Bottom Line

Hidden charges can turn an apparently low-cost loan into an expensive liability if they are not understood in advance. In India’s 2025 lending environment, RBI has significantly improved transparency by mandating Key Facts Statements, Actual cost of borrowing disclosure and fair penal charge practices.

However, regulation is only one side of the equation. Borrowers must:

- Look beyond the headline interest rate

- Evaluate the all-inclusive cost of the loan

- Pay attention to processing fees, GST, penalties and prepayment conditions

- Use the KFS as a reference document throughout the relationship

By carefully reviewing documentation and asking detailed questions before signing, borrowers can avoid most unpleasant surprises and keep borrowing costs under control.

FAQs

What are charges on a loan?

Loan charges are the additional costs borrowers pay apart from the interest rate. These include fees like processing charges, documentation fees, late payment penalties, EMI bounce charges, insurance premiums, and account maintenance fees. Such charges can be one-time or recurring and directly impact the overall borrowing cost.

Do loans have hidden fees?

Yes, many loans may include hidden fees that are not always visible in promotional advertisements. These charges often appear in the fine print of the agreement or in the Key Facts Statement. Hidden fees can increase the actual cost of borrowing significantly, even when the offered interest rate looks affordable.

How to avoid hidden fees in loans?

To avoid hidden fees, always read the Key Facts Statement (KFS), schedule of charges, and sanction letter carefully before accepting a loan. Ask the lender to clearly explain prepayment rules, late payment charges, and how GST affects the total cost. Comparing the total cost and charges across lenders helps identify which loan is truly cheaper overall.

How to check hidden fee in loans?

Hidden fees can be identified by reviewing documents such as the KFS, loan agreement, and disbursement statement. Borrowers should specifically ask about processing fees, bounce charges, foreclosure penalties, service taxes, and any mandatory insurance. If any charge is not mentioned in writing, borrowers can question or refuse it.