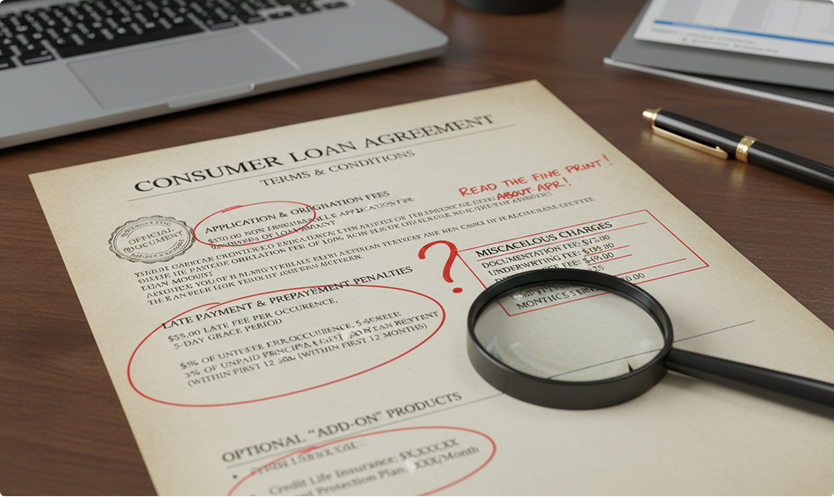

Hidden charges to watch out for in a loan

Hidden Charges to Watch Out for in a Loan

For most Indian borrowers, a loan is judged mainly by one number: the interest rate. However, in practice, the total cost of borrowing often depends just as much on the fees and hidden charges built into the loan structure.

With the rise of digital lending apps, BNPL products, personal loans, home loans, vehicle loans, and credit cards, small charges spread across the loan lifecycle can significantly increase the effective cost of credit. Many of these are not obvious at first glance and only appear in the fine print, schedules of charges, or repayment statements.

In response, the Reserve Bank of India (RBI) has tightened rules on Key Facts Statements (KFS), Actual cost of borrowing and penal charges, compelling lenders to disclose the all-inclusive cost of borrowing in a simple format for retail and MSME loans.

Even with stronger regulations, borrowers still need to understand which charges to look for and how they affect the overall cost.

This guide explains the major hidden charges to watch out for in a loan in India, how regulations work, and how borrowers can protect themselves before signing a loan agreement.

What Are Hidden Charges in a Loan?

Hidden charges are fees and costs associated with a loan that are not immediately obvious from the advertised interest rate. They may appear in:

- Sanction letters

- Fee schedules

- Loan agreements

- Disbursement statements

These charges may be one-time (for example, processing fees) or recurring (for example, penal charges or bounce fees). When added together, they can significantly increase the effective cost of borrowing, even if the nominal interest rate looks attractive.

Key Takeaways

- Hidden charges and loan hidden fees can significantly increase the total cost of borrowing, even when the advertised interest rate looks low.

- Always check the Key Facts Statement (KFS) and Actual cost of borrowing to understand the complete pricing structure; including processing fees, GST, penalties, and insurance.

- Extra costs such as prepayment and foreclosure charges, EMI bounce charges, penal interest, and documentation or legal fees can impact your monthly cash flow if not planned for.

- Borrowers should read the loan agreement carefully, ask questions about unclear items, and ensure every charge is disclosed upfront to avoid surprises later.

Why Hidden Charges Matter for Indian Borrowers

For many borrowers, especially in Tier-2 and Tier-3 cities, small differences in EMI or one-time charges can materially impact monthly cash flows.

Hidden charges matter because they can:

- Increase the effective interest rate well beyond the headline rate

- Reduce the actual amount credited to the borrower’s account after deductions

- Make prepayment or foreclosure more expensive than expected

- Add costs in case of temporary cash-flow stress (e.g., penal and bounce charges)

With more Indians relying on EMIs, credit cards, digital loans and BNPL, awareness of fee structures has become a key part of responsible borrowing.

Key Regulatory Safeguards

1. Key Facts Statement (KFS) and Actual cost of borrowing Disclosure

RBI has made Key Facts Statements (KFS) mandatory for all retail and MSME term loans, requiring lenders to present key loan terms, including the all-inclusive Actual cost of borrowing, in a standard, easy-to-understand format.

Important points:

- Actual cost of borrowing must include interest plus all fees and charges, including third-party charges that are recovered by the lender (insurance, legal, etc.).

- Any fee or charge not mentioned in the KFS cannot be charged later.

This gives borrowers a strong legal basis to question unexpected charges.

2. Penal Charges Regime

RBI has clarified that penalties for non-compliance with loan terms must be levied as “penal charges” and not as “penal interest”. Penal charges cannot be added to the rate of interest, and no interest can be compounded on penal charges.

Lenders must ensure: Penal charges are reasonable, transparent and non-discriminatory within a product category.

3. Prepayment / Foreclosure Rules

RBI has long disallowed prepayment penalties on floating-rate home loans for individual borrowers.

In 2025, RBI further tightened rules by prohibiting prepayment charges on floating-rate loans to individuals for non-business purposes, with broader applicability from 1 January 2026.

This means:

- Floating-rate home loans to individuals already enjoy no prepayment penalties.

- For other floating-rate loans to individuals (e.g., certain personal or education loans), the new “no prepayment charge” rule will fully apply prospectively from 2026; however, many lenders have already started aligning policies ahead of time.

4. GST on Loan Charges

Interest on loans is not subject to GST, but most fees and service charges are, typically at 18%.

This means the effective cost of each fee is higher than the base amount alone.

Common Hidden Charges in Loans

Processing Fees and GST

Processing fees are among the most common upfront charges. These are typically:

- A percentage of the loan amount (for example, 1-3% for many personal loans)

- Deducted from the sanction at disbursement, so the borrower receives less than the approved amount

On top of this fee, 18% GST is charged on the processing amount.

For example, on a Rs 5 lakh personal loan with a 3% processing fee:

- Processing fee = Rs.15,000

- GST @18% on fee = Rs.2,700

- Net credit to the borrower = Rs 4,82,300

The EMIs, however, are calculated on the full Rs 5 lakh principal, not the net credit.

Documentation, Legal and Valuation Charges

For home loans and loans against property, additional charges often include:

- Legal scrutiny fees for verifying title documents

- Valuation fees for property assessment

- Stamp duty and registration charges (where applicable)

These may be charged on an actual basis and must form part of the Actual cost of borrowing and be disclosed in the KFS if recovered by the lender.

Prepayment, Foreclosure and Part-Prepayment Charges

Depending on the loan type and nature of the interest rate:

- Floating-rate home loans to individuals: No prepayment/foreclosure penalties permitted.

- Other floating-rate loans to individuals: RBI directions in 2025 further limit prepayment charges, with full effect from January 2026.

- Fixed-rate loans and some NBFC products: Prepayment and foreclosure charges may still apply, especially in the first few years of the loan.

Borrowers should check:

- Whether prepayment is allowed partially or fully

- Whether there is a lock-in period (e.g. no prepayment for 12-24 months)

- The percentage charged on the outstanding amount (for example, 2-5%)

- Whether GST is applied on the prepayment fee (commonly at 18%)

Penal Charges and Late Payment Fees

When an EMI is delayed or terms are violated, lenders levy penal charges. After RBI’s 2023 circular:

- Penal charges cannot be simply added as extra interest; they must be shown separately.

- No compounding of penal charges is allowed.

However, these charges can still be substantial in practice, often expressed as:

- A fixed amount per month of default, or

- A percentage per annum on the overdue amount (for example, 24% p.a., charged as a monthly penalty)

Penal charges also generally attract GST.

EMI Bounce / Mandate Failure Charges

If an EMI is unpaid due to insufficient balance or technical failure, lenders may charge:

- Cheque bounce charges

- ECS/NACH/mandate failure charges

- Additional penal charges on overdue EMIs

These charges can range from a few hundred to over a thousand rupees per bounce in many retail products.

Repeated bounces not only increase costs but also negatively affect the credit profile and CIBIL score.

Conversion, Restructuring and Rate-Reset Fees

Many lenders charge fees for:

- Interest rate conversion (for example, moving from fixed to floating)

- Spread reduction (reducing the margin over benchmark for an existing home loan)

- Tenure changes or restructuring

These are sometimes marketed as “conversion offers” or “rate negotiation options” but are effectively chargeable services. They must form part of the loan’s overall cost disclosure when availed.

Insurance Bundled with Loans

It is common for lenders or partners to bundle:

- Credit life insurance

- Health or accident cover

- Property insurance (for secured loans)

When the lender recovers premium amounts, these must be part of Actual cost of borrowing and KFS, and borrowers are entitled to:

- Know whether insurance is optional or mandatory

- See separate documentation and receipts for premiums paid

Borrowers should confirm whether alternate policies are allowed and avoid feeling compelled into products that do not serve their needs.

Statement, Account Maintenance and Other Administrative Fees

Additional charges may include:

- Duplicate statement/interest certificate charges

- Loan account maintenance fees

- Re-issuance of amortisation schedules

- Copy of documents charges

Individually, these may appear small, but repeated usage can add up over the tenure.

How to Spot Hidden Charges Before Taking a Loan

To avoid unpleasant surprises:

- Read the KFS carefully

- Confirm Actual cost of borrowing, including all fees.

- Check whether any “other charges” are mentioned generically, ask for specifics.

- Request and review the Schedule of Charges: Processing fee, bounce charges, penal charges, statement fees, conversion fees etc.

- Examine the sanction letter and loan agreement: Look for clauses on prepayment, foreclosure, part-payment rules and lock-in periods.

- Ask for a “net disbursal illustration”: Approved amount vs. amount credited after all upfront deductions.

- Clarify tax treatment: Confirm where 18% GST is applicable and estimate the total impact.

All these documents should be provided in a language and format that borrowers can understand, as emphasised by RBI’s guidelines on KFS and transparency.

Checklist Before Signing a Loan Agreement

Before signing:

- Confirm the exact processing fee and GST impact

- Check whether any non-refundable upfront fees apply

- Understand prepayment and foreclosure rules clearly

- Note all penal charges, bounce fees and administrative charges

- Clarify if insurance is optional and whether alternative insurers are allowed

- Ensure all charges match what is disclosed in the KFS and sanction letter

- Retain copies of all signed documents, acknowledgements and receipts

If any fee appears at a later stage that was not mentioned in the KFS or sanction letter, borrowers can challenge it under the RBI’s fair lending and disclosure norms.

The Bottom Line

Hidden charges can turn an apparently low-cost loan into an expensive liability if they are not understood in advance. In India’s 2025 lending environment, RBI has significantly improved transparency by mandating Key Facts Statements, Actual cost of borrowing disclosure and fair penal charge practices.

However, regulation is only one side of the equation. Borrowers must:

- Look beyond the headline interest rate

- Evaluate the all-inclusive cost of the loan

- Pay attention to processing fees, GST, penalties and prepayment conditions

- Use the KFS as a reference document throughout the relationship

By carefully reviewing documentation and asking detailed questions before signing, borrowers can avoid most unpleasant surprises and keep borrowing costs under control.

FAQs

What are charges on a loan?

Loan charges are the additional costs borrowers pay apart from the interest rate. These include fees like processing charges, documentation fees, late payment penalties, EMI bounce charges, insurance premiums, and account maintenance fees. Such charges can be one-time or recurring and directly impact the overall borrowing cost.

Do loans have hidden fees?

Yes, many loans may include hidden fees that are not always visible in promotional advertisements. These charges often appear in the fine print of the agreement or in the Key Facts Statement. Hidden fees can increase the actual cost of borrowing significantly, even when the offered interest rate looks affordable.

How to avoid hidden fees in loans?

To avoid hidden fees, always read the Key Facts Statement (KFS), schedule of charges, and sanction letter carefully before accepting a loan. Ask the lender to clearly explain prepayment rules, late payment charges, and how GST affects the total cost. Comparing the total cost and charges across lenders helps identify which loan is truly cheaper overall.

How to check hidden fee in loans?

Hidden fees can be identified by reviewing documents such as the KFS, loan agreement, and disbursement statement. Borrowers should specifically ask about processing fees, bounce charges, foreclosure penalties, service taxes, and any mandatory insurance. If any charge is not mentioned in writing, borrowers can question or refuse it.