How to report fraud loan apps

How to Report Fraud Loan Apps in India: A Step-by-Step Guide for Borrowers

Fraud Loan Apps have become one of the most common triggers of digital financial stress in India. These apps often promise instant approvals, zero paperwork, and quick cash, but the real goal is usually data theft, illegal recovery tactics, hidden charges, or outright fraud. Borrowers may face harassment, public shaming, and threats after installing the app or sharing basic KYC details.

Knowing how to Report Loan Fraud quickly can reduce financial loss and help stop further misuse of personal data. India’s reporting ecosystem in today’s date includes the National Cyber Crime Helpline 1930, the National Cyber Crime Reporting Portal, local cyber police stations, and formal complaint systems for cases involving RBI regulated entities. RBI has also enabled public verification tools to help citizens confirm whether a digital lending app is actually linked to a regulated lender.

This guide explains what fraud loan apps look like, what to do immediately, where to report, and how to build a strong complaint with the right evidence.

What Is a Fraud Loan App?

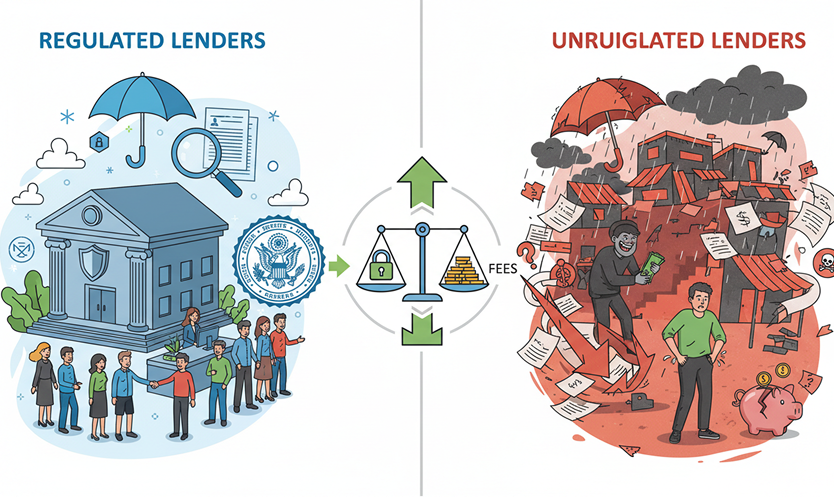

A fraud loan app is a digital app that pretends to offer loans but works in a dishonest way. Some of these apps are completely illegal and are not connected to any bank or NBFC regulated by RBI. Others falsely use well-known names or wrongly claim to be linked to RBI-regulated lenders. Such apps can lead to problems like loans taken without consent, misuse of personal data, hidden charges, repeated loan renewals, and aggressive or abusive recovery practices.

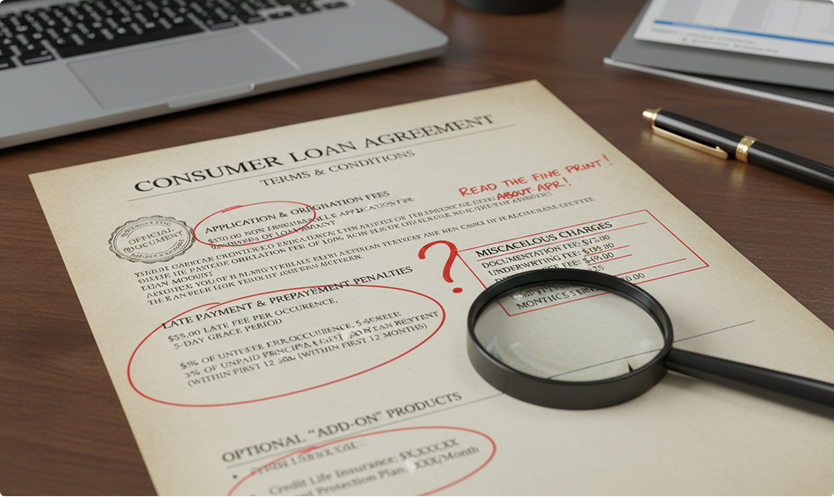

As per RBI rules, all digital loans must be given by regulated lenders, and borrowers must clearly receive details like interest rate, fees, tenure, and total repayment amount through a Key Fact Statement. Any loan app that does not follow these basic rules should be treated as risky and avoided.

Key Takeaways

- Report cyber financial fraud immediately using 1930 and the National Cyber Crime Reporting Portal to improve the chance of fund recovery.

- If a regulated bank or NBFC is involved, complaints can also be filed through RBI’s Complaint Management System under the Integrated Ombudsman Scheme.

- RBI has operationalized a public directory of Digital Lending Apps deployed by RBI regulated entities (from July 1, 2025) to help borrowers verify legitimacy.

- Fraud loan apps commonly rely on coercion, hidden fees, and invasive permissions like contact access.

- Evidence quality matters. Screenshots, call logs, payment proofs, and app details make complaints stronger.

How Fraud Loan Apps Typically Operate

Fraud loan apps usually follow one or more of these patterns:

Data-first fraud

The app asks for Aadhaar, PAN, selfies, contacts, and storage access. The loan may be small or may not be disbursed at all. The goal is often extortion, impersonation, or identity misuse.

Fee-first fraud

The app approves a loan instantly but demands a “processing fee” or “verification fee” upfront. After payment, the app disappears or blocks the user.

Disbursal-trap fraud

A small amount is disbursed, but the repayment demand is inflated through hidden charges, short tenures, and aggressive penalties.

Harassment-led recovery

The app threatens to message contacts or post personal data. RBI’s digital lending framework emphasizes consent-based data practices and fair conduct expectations in loan journeys, which such apps violate.

Immediate Steps to Take Before Reporting

Speed matters. Taking these steps first can limit damage.

Immediate safety actions

- Stop further payments to unknown personal accounts or UPI IDs.

- Take screenshots of the app screens, loan details, repayment demands, and threats.

- Save call recordings if legally permissible and available on the device.

- Block the app from permissions, especially contacts, SMS, photos, microphone, and storage.

- If money was transferred, contact the bank immediately and report unauthorized transactions.

Do not delete the app immediately

Keep the app installed until key evidence is captured, including app name, developer, registered contact details shown inside the app, and transaction references.

Where to Report Fraud Loan Apps in India

Reporting should follow a layered approach: cyber fraud reporting, law enforcement escalation, and regulator escalation if a regulated lender is involved.

Official reporting channels:

- Cyber Crime Helpline 1930: Immediate action for rapid reporting of online financial fraud and attempted fund recovery

- National Cyber Crime Reporting Portal (NCRP): Formal complaint for online complaint registration for cybercrime, including financial fraud

- Local Cyber Crime Police Station / FIR: Strong legal action for investigation, notices to banks, device and account tracing

- RBI CMS under Integrated Ombudsman Scheme: If a regulated entity is involved for complaints against regulated entities for deficiency in service

- RBI Sachet Portal: Direction to the right authority, provides pathways for cyber fraud reporting and regulator routing

Step-by-Step: How to File a Complaint on 1930 and the NCRP Portal

Step 1: Call 1930 immediately

- Provide transaction details, bank name, UPI reference, and timeline.

- The goal is to initiate fast action so suspect accounts can be flagged quickly.

Step 2: File a complaint on the National Cyber Crime Reporting Portal

Typical information required includes:

- Victim details (name, mobile, email)

- Incident type (financial fraud, identity misuse)

- Fraud app details (name, store listing, website if any)

- Transaction details (UPI, account number, reference IDs)

- Evidence uploads (screenshots, chat logs, call logs)

The portal exists to help citizens report cyber crimes online and supports financial fraud reporting linked to 1930.

Step 3: Visit the cyber cell for FIR if threats or large losses exist

FIR is advisable when:

- repeated harassment occurs

- money loss is high

- identity theft is suspected

- fake loans were created using stolen KYC

- there are threats of violence or public shaming

If the App Claims a Bank or NBFC Partner

Fraud apps often claim “RBI approved” or display a bank or NBFC logo. In such cases, verification becomes critical.

What to do:

- Ask for the name of the bank or NBFC that is actually giving the loan.

- Ask for the Key Fact Statement that clearly shows interest rate, fees, loan period, and total amount to be repaid. RBI rules require this for digital loans.

- If a regulated lender’s name is mentioned, raise a complaint with that lender first. If the issue is not solved, it can be escalated to RBI through the CMS system.

RBI allows complaints against banks and NBFCs under its Integrated Ombudsman Scheme using the CMS portal.

Evidence Checklist to Strengthen the Complaint

- App identity proof: App name, screenshots of listing, developer details, app version

- Loan details: Sanction screen, repayment schedule, “due now” screen, penalties shown

- Threat proof: Screenshots of WhatsApp/SMS threats, call recordings where available

- Payment proof: UPI reference numbers, bank statements, transaction IDs

- Device proof: Permission screens showing contact access, storage access requests

- KYC misuse proof: Any alerts about new loans or accounts opened without consent

How to Verify Whether a Loan App Is Linked to a Regulated Lender

RBI has operationalized a public directory of Digital Lending Apps deployed by regulated entities to help customers verify whether an app is actually tied to an RBI regulated lender.

Verification steps:

- Search the app name against RBI’s DLA directory.

- Check whether the lender named inside the app is a regulated entity.

- If the app is not listed but claims affiliation, treat it as suspicious and report it.

Common Red Flags That Confirm a Loan App Is Fraudulent

- Upfront fees demanded before disbursal

- Loan approval without any meaningful checks

- No Key Fact Statement or unclear cost disclosure

- Requests for contact list access

- Threat messages to contacts or public shaming tactics

- Repayment due within 3 to 10 days with inflated charges

- “RBI approved” claims without naming a regulated entity

- Payments requested to personal accounts

Safe Borrowing Checklist for the Future

- Use loan apps only from known banks or NBFCs that are registered with RBI.

- Check the app name in RBI’s list of approved digital lending apps if there is any doubt.

- Avoid apps that ask for access to contacts or personal phone data.

- Always ask for a Key Fact Statement that clearly shows interest rate and total repayment amount.

- Never send processing fees to personal UPI IDs or unknown accounts.

- Read repayment dates and loan duration carefully, especially for short-term loans.

The Bottom Line

Fraud Loan Apps are designed to exploit urgency, limited awareness, and digital trust. Reporting quickly is the strongest protection. The most effective first step is to call 1930 and lodge a complaint on the National Cyber Crime Reporting Portal so financial fraud response mechanisms can begin early.

If a regulated bank or NBFC is involved, escalation through RBI’s complaint system under the Integrated Ombudsman framework adds an additional layer of accountability.

RBI’s public directory of digital lending apps deployed by regulated entities makes verification easier, but caution remains essential.

FAQs

How to complain about fake loan app?

In India, the primary route to complain about a fake loan app or any online financial fraud is through the National Cybercrime Reporting Portal (www.cybercrime.gov.in) using the Citizen Financial Cyber Fraud Reporting and Management System. Citizens can also call the Indian Cybercrime Helpline 1930 to report instant cyber fraud including fake loan apps and unauthorized transactions. You can upload relevant evidence such as screenshots, transaction proofs, app details, and communication records when filing the complaint online. If threats, extortion, or identity misuse occur, you can also visit your nearest cyber police station to file an FIR.

How to complain to RBI against fraud loan app?

The Reserve Bank of India’s complaint system is intended for issues involving RBI regulated entities (like banks or registered NBFCs). If a loan app claims association with a bank or NBFC and you suspect misconduct by the regulated entity, you can file a grievance through the RBI Complaint Management System (CMS) under the Integrated Ombudsman Scheme. However, for fraud loan apps that are unregulated and not linked to an RBI regulated lender, the appropriate first step is reporting to the National Cybercrime Reporting Portal or local cyber police. RBI itself has also coordinated with cybercrime authorities to monitor and help act against illegal digital lending platforms.

How do I get my money back from online fraud in India?

Recovering funds after an online fraud is not guaranteed, but acting quickly improves chances. Immediately call the 1930 cybercrime helpline and file a complaint on the National Cybercrime Reporting Portal with transaction details (bank/UPI reference, amount, date/time) to trigger coordinated action by law enforcement and banks. Also inform your bank or payment service provider promptly to block further unauthorized transactions and request investigation. In some cases, the cybercrime system may identify and freeze suspect accounts if the complaint is lodged early.

How do you report an app for fraud?

There are two aspects to reporting an app for fraud: platform-level and government-level. Platform-level: If it’s on the Google Play Store, open the app’s page, use the Flag as inappropriate option, select the reason (fraud, malware, etc.), and submit. This helps platform moderators review and potentially remove the app. Government-level: Report the fraudulent app via the Indian Cybercrime Helpline (1930) or the National Cybercrime Reporting Portal (cybercrime.gov.in) under online financial fraud/cybercrime. Upload evidence like screenshots, transaction details, and any threatening messages to assist investigation and enforcement. For regulated lenders, complaints can also be escalated through RBI’s CMS if the app misrepresented a regulated partner.