What are regulated vs unregulated lenders?

Regulated Lenders vs Unregulated Lenders: What Indian Borrowers Must Know About

India’s rapid shift toward digital borrowing has made credit more accessible than ever. Millions now apply for personal loans, small business loans, and instant credit through mobile apps, fintech platforms, banks, and NBFCs. But with this accessibility comes confusion about who is allowed to lend legally. As a result, many borrowers unknowingly take loans from unregulated lenders, exposing themselves to high charges, harassment, and fraud.

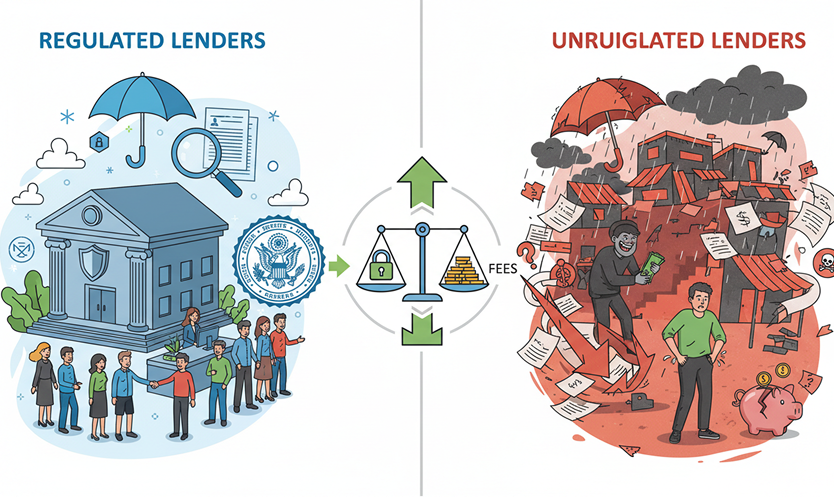

Understanding the difference between Regulated Lenders and Unregulated Lenders is essential for safe borrowing. Regulated lenders follow strict rules issued by the Reserve Bank of India (RBI), while unregulated lenders operate outside legal frameworks and pose financial and legal risks.

This guide explains the definitions, differences, risks, benefits, red flags, and how to verify if a lender is legitimate.

What Are Regulated Lenders in India?

Regulated lenders are financial institutions that are officially supervised, licensed, and governed by the RBI or other statutory bodies. They must follow strict rules on interest rates, disclosures, recovery practices, customer protection, and grievance redressal.

Regulated lenders include:

- Scheduled Commercial Banks: Large public and private banks regulated by RBI that accept deposits and provide loans, credit cards, and other banking services to individuals and businesses.

- Co-operative Banks: Member-owned banks formed by groups such as local communities, farmers, traders, or small businesses, offering banking and lending services under a co-operative structure.

- RBI Registered NBFCs: Non-banking financial companies registered with RBI that provide loans, credit, leasing, and other financial services but do not hold demand deposits like regular banks.

- Housing Finance Companies (HFCs): Specialised financial institutions that primarily provide home loans and loans against property for housing-related purposes under housing finance regulations.

- Microfinance Institutions (MFIs): Institutions that offer small-ticket loans to low-income individuals, self-help groups, and micro-entrepreneurs, often in rural and semi-urban areas, to support livelihood activities.

- Payment Banks / Small Finance Banks: Niche banks licensed by RBI; payment banks focus on small savings and payments, while small finance banks provide basic banking and lending services to underserved and low-income segments.

Compliance Requirements for Regulated Lenders in India

- RBI Fair Practices Code: A mandatory framework that ensures lenders treat borrowers fairly, follow transparent processes, disclose terms clearly, and avoid misleading practices.

- Digital Lending Guidelines: Rules governing app-based and digital loan journeys, including mandatory disclosures, consent-based data access, clear grievance mechanisms, and restrictions on third-party collection agents.

- Data Protection and KYC Norms: Lenders must securely handle customer data, follow privacy standards, complete KYC verification, and prevent misuse of personal information.

- Transparent Interest and Fee Disclosures: All regulated lenders must clearly reveal interest rates, processing fees, penalty charges, and total loan cost before disbursal to ensure informed borrowing.

- Ethical Recovery Practices: Lenders must follow strict RBI rules on collections, including no harassment, no threatening behaviour, restricted calling hours, and training of recovery agents.

Borrowers who choose regulated lenders are legally protected and have access to formal grievance systems.

Key Takeaways

- Regulated lenders are authorised by the RBI and must comply with lending and collection rules.

- Unregulated lenders have no oversight and frequently violate laws through excessive interest, abusive collection, and misuse of personal data.

- Borrowing from regulated lenders protects borrowers from fraud, data leaks, and harassment.

- The RBI publishes official lists of all registered NBFCs and authorised lenders.

- Loan apps must disclose the name of the regulated entity underwriting the loan.

Categories of Regulated Lenders in India

Banks

Includes public sector banks, private banks, and small finance banks. They offer personal loans, home loans, business loans, and credit lines with strict underwriting and compliance requirements.

RBI-Registered NBFCs (Non-Banking Financial Companies)

These are major players in digital lending. They follow RBI rules on:

- Interest rate transparency

- Capital adequacy

- Fair practices

- Recovery norms

Housing Finance Companies (HFCs)

Regulated under a combination of RBI norms and sector-specific guidelines.

Microfinance Institutions (MFIs)

Offer small-ticket loans with regulated pricing caps and structured repayment methods.

Co-operative Banks

Subject to dual regulation but still operate under formal lending norms.

All these entities operate within a regulated ecosystem ensuring borrower safety.

What Are Unregulated Lenders?

Unregulated lenders operate without RBI authorisation and without adherence to any legal lending framework.

How Unregulated Lenders Commonly Appear in India:

- Illegal Loan Apps: Mobile applications offering instant loans without RBI approval, often charging extremely high interest rates and using abusive recovery tactics.

- Private Moneylenders: Individuals or small groups lending money without any licence or regulatory oversight, usually at very high interest rates and informal terms.

- Unregistered Digital Finance Platforms: Websites or apps posing as “fintech lenders” but not registered with RBI; they operate without compliance norms or consumer protections.

- Social Media Lenders: Individuals or anonymous groups offering loans through platforms like Facebook, Instagram, or YouTube, usually demanding upfront fees or access to personal data.

- Informal Lenders on WhatsApp/Telegram Groups: Loan providers circulating offers through messaging groups, often requesting Aadhaar/PAN copies and then misusing personal information for fraud or extortion.

Unregulated lenders charge extremely high interest, impose hidden fees, and often misuse borrower data for intimidation.

Activities Unregulated Lenders Are Not Allowed to Engage In

- Offer loans to the public: Only RBI-licensed banks, NBFCs, and regulated institutions are legally permitted to lend. Unregulated entities cannot offer credit under Indian law.

- Collect payments using threats: Harassment, intimidation, blackmail, and public shaming violate RBI recovery rules and Indian laws related to criminal intimidation and extortion.

- Access borrower phone contacts: Accessing contacts without consent breaches data protection norms and privacy laws. It is prohibited under digital lending guidelines.

- Pose as RBI-approved entities: Misrepresenting themselves as “RBI registered”, “government approved”, or “official finance partners” is illegal and considered fraudulent activity.

Any lending activity outside the RBI’s regulatory scope is considered illegal.

Risks of Borrowing from Unregulated Lenders

Borrowing from unregulated lenders exposes customers to significant financial and legal risks.

Excessive Interest and Hidden Charges

Interest can exceed 200 percent annually with add-on fees deducted upfront.

Data Theft and Misuse

Many illegal loan apps demand access to contacts, photos, and messages, later using this data for blackmail.

Harassment and Threatening Recovery

Borrowers often face:

- Mental harassment

- Threat calls

- Public shaming

- Use of fake police notices

Lack of Legal Protection

Borrowers cannot seek RBI support or Ombudsman intervention because the lender itself is illegal.

Financial Fraud

Funds may not be disbursed even after approval fees. Many apps shut down after collecting upfront payments.

Identity Theft

Borrower KYC documents may be misused for further fraud.

These risks make unregulated lending extremely dangerous.

How to Verify if a Lender Is Regulated

Borrowers can take simple steps to confirm the legitimacy of any lender.

- Check the RBI list: Verify whether the NBFC or bank appears in the official RBI directory.

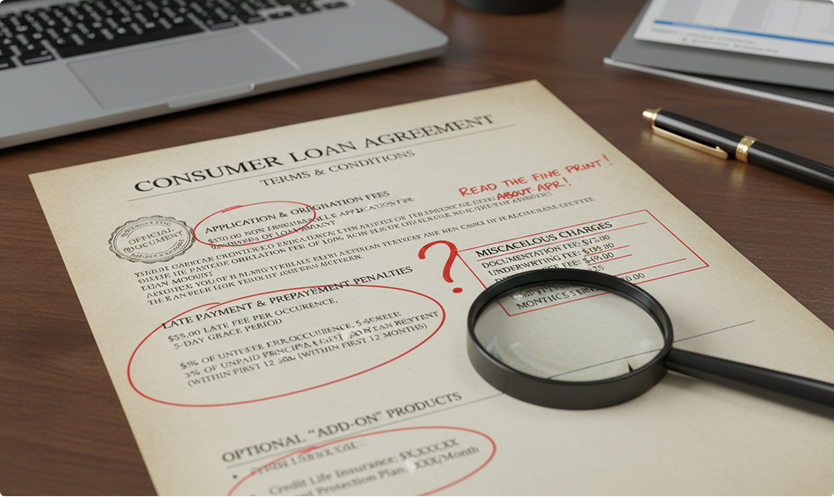

- Check the loan agreement: The agreement must clearly state the regulated entity underwriting the loan.

- Review the website: A legitimate lender displays company name, registered address, certificate of registration, and grievance contact details.

- Look for the Key Fact Statement: Mandatory for every digital loan.

- Avoid lenders who: Ask for upfront fees, have no physical office, withhold information, access phone contacts, or pressure borrowers into quick disbursal.

If a lender seems suspicious, it is safer to leave immediately.

Warning Signs of Unregulated Lenders

Borrowers should avoid lenders showing these red flags:

- No RBI registration

- No loan agreement

- Excessive permissions on the app

- High processing fees deducted upfront

- Interest rates not disclosed

- Use of aggressive language

- Fake government symbols

- No customer care details

- Payments demanded via personal accounts

If any two or more signs appear, the lender is likely unregulated.

Safe Borrowing Checklist for Indian Consumers

Before taking any loan, always verify:

- Is the lender listed on the RBI website?

- Does the app disclose the NBFC or bank partner?

- Are charges and APR clearly shown?

- Is the loan agreement shared immediately?

- Is customer support reachable?

- Are recovery practices ethical?

Borrowers should avoid shortcuts that compromise financial and personal safety.

The Bottom Line

Borrowers in India have two choices: Regulated Lenders, which follow RBI rules and offer transparent, legally compliant credit, and Unregulated Lenders, which operate outside the law and expose borrowers to harassment, fraud, and financial exploitation. In a growing digital lending ecosystem, distinguishing between the two is essential for safe and responsible borrowing.

Choosing a regulated lender protects borrowers from data misuse, excessive pricing, and unethical recovery while ensuring access to proper grievance redressal. As India continues to strengthen digital lending regulations, awareness remains the most effective defence. Borrow smart, choose formal credit sources, and avoid lenders who operate in the shadows.

FAQs

What are the latest RBI loan rules?

The latest RBI loan rules focus on safer digital lending, transparent disclosures, ethical recovery, and data protection. Lenders must clearly disclose APR, charges, tenure, and total repayment before disbursal. All digital lending apps must be linked to a regulated bank or NBFC. Recovery agents must follow strict conduct guidelines and cannot harass or threaten borrowers. Borrower data can only be collected with consent and cannot be misused or shared with third parties. These rules aim to protect borrowers from hidden charges and illegal loan apps.

What is the new loan policy?

The new loan policy enhances borrower protection in both physical and digital lending. It mandates standardized Key Fact Statements, transparent cost disclosures, limited access to customer data, and proper grievance redressal systems. High risk unsecured lending is monitored more closely, and lenders must strengthen credit assessments. Loan collection activities are limited to specific hours, and lenders must record agent details for accountability. The policy aims to reduce borrower distress and improve responsible lending across India.

What are the latest banking guidelines?

The latest banking guidelines emphasize stronger risk management, responsible retail lending, fair collection practices, and upgraded KYC and data privacy systems. Banks must ensure accurate APR display, clear loan agreements, and customer consent for digital data use. Collections must follow RBI’s code of conduct. Banks are also required to monitor unsecured loan portfolios more carefully and prevent overexposure among high risk borrowers. The guidelines aim to increase transparency and reduce customer complaints.

What is the difference between regulated and unregulated lending?

Regulated lending is carried out by banks, NBFCs, microfinance institutions, housing finance companies, and small finance banks that operate under RBI rules. They must follow strict norms for interest disclosures, KYC, data privacy, recovery conduct, and grievance handling. Unregulated lending is conducted by illegal loan apps, private moneylenders, social media lenders, and platforms not registered with RBI. They often charge excessive interest, hide fees, misuse personal data, and use aggressive recovery tactics. Regulated lenders provide legal protections, while unregulated lenders expose borrowers to financial and personal risk.