What is a personal loan?

Personal Loan: What It Is, How It Works, and How to Use One Responsibly in India

A personal loan has become one of the most widely used credit options in India, offering individuals quick access to funds without needing any collateral. Whether it is a medical emergency, a sudden expense, or a planned purchase, an instant loan can provide timely financial support when savings fall short. In simple terms, a personal loan refers to borrowing a fixed amount from a bank, NBFC, or regulated digital lender and repaying it through monthly EMIs over a chosen tenure. With seamless online applications, quick approvals, and faster loan disbursal, instant personal loans are now a convenient solution for salaried and self-employed borrowers alike.

However, responsible borrowing is crucial. Understanding personal loan interest rates, eligibility requirements, EMI calculations, and overall repayment capacity helps ensure the loan supports financial stability rather than creating future stress. This guide explains how personal loans work in India, their benefits, risks, and smart ways to use them effectively.

What Is a Personal Loan?

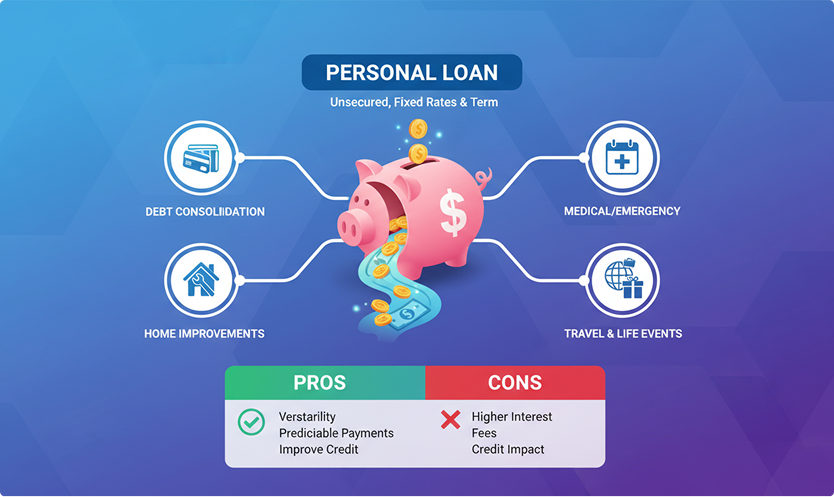

A personal loan is a fixed amount of money borrowed from a bank, NBFC, or digital lender to meet personal financial needs. Borrowers repay the loan in equated monthly installments (EMIs) over a defined tenure with interest.

In India, most personal loans are unsecured, meaning no collateral such as property, gold, or deposits is required. Instead, lenders assess credit score, income, employment stability, and existing liabilities to determine eligibility and pricing.

Personal loans are commonly used for medical emergencies, education top-ups, rent deposits, weddings, and short-term cash flow gaps. They may also be used to consolidate higher-cost debts into a single structured EMI.

Key Takeaways

- Personal loans in India are mostly unsecured and repaid via fixed EMIs.

- Interest rates vary widely, generally from ~9-24% per year depending on risk profile.

- Fintech NBFCs dominate small-ticket personal loan volumes through digital journeys.

- Rapid growth in unsecured credit requires borrowers to assess repayment capacity carefully to avoid debt stress.

- Best used for emergencies and planned necessities rather than recurring consumption.

How Personal Loans Work in India

Borrowers apply online or offline by submitting income and identity documents. Lenders evaluate:

- Credit score and repayment history

- Income and employer category

- Existing EMIs and debt-to-income ratio

If approved, the loan amount (less fees) is disbursed to the bank account. EMI payments start in the following billing cycle through auto-debit.

EMIs consist of both interest and principal, the interest portion is higher during initial months and reduces over time.

Common Features of Personal Loans

Unsecured Structure

No collateral is pledged in most personal loans. As lender risk increases, pricing tends to be higher than secured loans.

Fixed EMIs and Tenure

- Usual tenures: 12-60 months, with some lenders extending up to 84 months

- EMI remains constant for better budgeting

Interest Rate Range

- Prime salaried customers: 9-16% per annum

- Higher-risk or small-ticket digital loans: 22-36%+ per annum

Pricing varies depending on credit profile, income stability, and customer relationship.

Loan Amount Range

- ₹25,000-₹50,000 minimum via fintech platforms

- Up to ₹25-40 lakh for strong salaried borrowers with banks

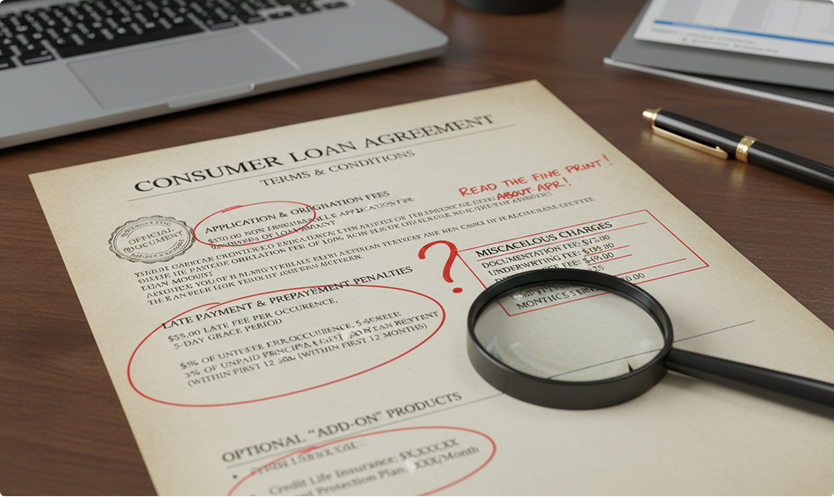

Fees and Charges

- Processing fees: ~0.5-3% + GST

- Prepayment/foreclosure charges may apply

- Penalty interest and bounce charges on missed EMIs

End-Use Flexibility

Funds may be used for most legal personal needs without detailed monitoring from the lender.

Size of India’s Personal Loan Market

Personal loans account for a rising share of unsecured retail credit.

- Outstanding balance of scheduled commercial banks is approximately ₹10.3 lakh crore as of March 2025.

- The GNPA ratio increased from 1.03% to 1.18% between March 2024 and March 2025.

- Unsecured retail GNPA rose from 1.56% to 1.82% during the same period

Fintech NBFCs are driving growth in small-ticket lending.

- Around 10.9 crore personal loans were sanctioned worth ₹1.06 lakh crore in FY 2024–25

- They represent about 74 percent of loan accounts by volume, but only around 12 percent by value

Household leverage has increased to a low 40 percent of GDP, indicating greater dependence on credit.

When a Personal Loan Makes Sense

A personal loan can be suitable when:

- Handling medical emergencies or unavoidable expenses

- Bridging short-term liquidity gaps with future income visibility

- Consolidating high-cost debt like revolving credit card balances

- Funding education or professional upgrades that improve earnings potential

It may be inappropriate when:

- Funding frequent discretionary spending

- Using new loans to service existing loan EMIs

- Total EMIs exceed 40-45% of monthly net income

Risks of Personal Loans

Higher Borrowing Cost

Interest rates exceed most secured loans such as home loans or loans against assets.

Credit Score Impact

Late or missed EMIs negatively affect future loan access and cost.

Systemic Stress

Rising NPAs in unsecured retail loans point to increasing segment risk.

Household Over-Borrowing

Growing reliance on unsecured credit can constrain savings and reduce resilience to income shocks.

Eligibility and How to Qualify

Common criteria include:

Age: 21-60 years

Credit Score: ~700+ for best rates

Income: Minimum net monthly income threshold (varies by city)

Employment Stability: Minimum months with current employer or business vintage

Debt-to-Income Ratio: EMIs ideally <40-45% of net income

Required documents generally include Aadhaar, PAN, salary slips, Form 16, bank statements, or IT returns.

How to Apply for a Personal Loan in India

Step-by-step:

- Determine the required amount and purpose

- Check the credit report and correct any discrepancies

- Compare offers across banks, NBFCs, and digital lenders

- Keep KYC + financial documents ready

- Submit application (online/offline)

- Complete verification and sign agreement

- Loan amount is disbursed, EMIs commence

Pre-approved offers from existing banks/NBFCs often give quicker disbursal with minimal friction.

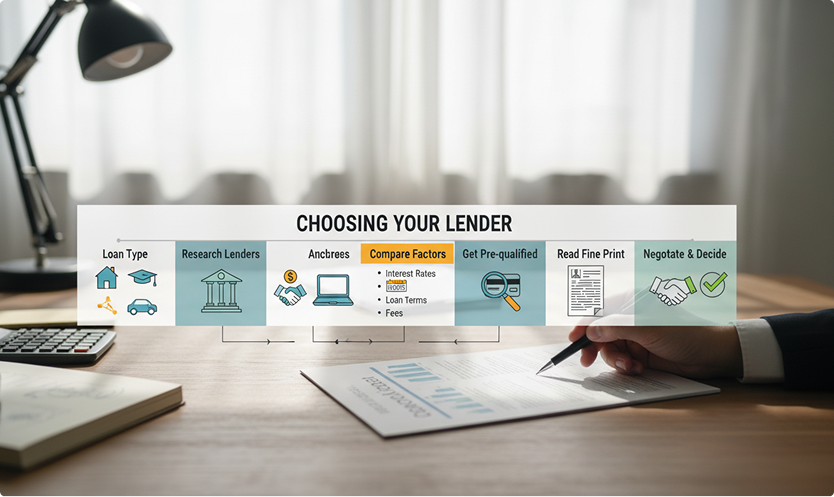

Comparing Personal Loan Lenders

Evaluate:

- Interest rate: Check how much interest is charged on the loan.

- Processing fees and prepayment rules: Look at upfront fees and whether early repayment is allowed without heavy charges.

- EMI affordability and tenure flexibility: Ensure the monthly EMI fits comfortably within income and the tenure is flexible.

- Minimum credit score or income requirement: Check eligibility conditions to avoid rejection.

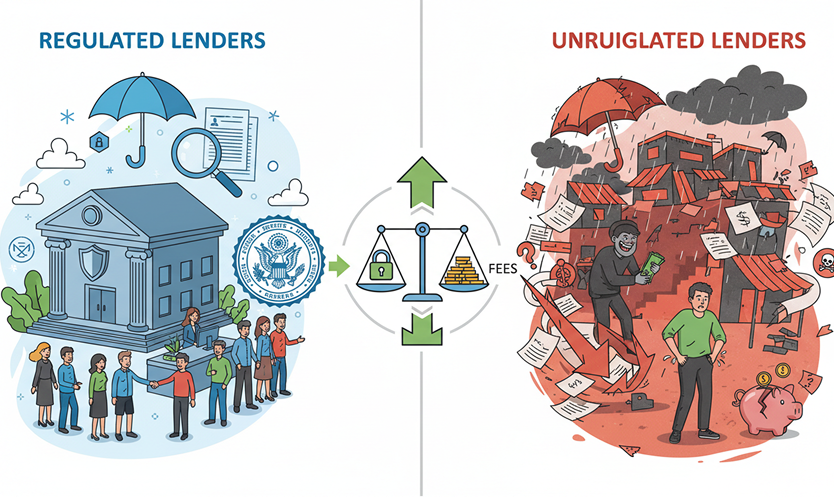

- Credibility, regulation, and customer service: Prefer banks or RBI-registered NBFCs with reliable support.

- Transparency of terms and recovery practices: Terms should be clear, and collection methods should be fair.

A slightly higher interest rate from a well-regulated lender is often safer than a cheaper loan from a risky or unregulated source.

FAQs

What is meant by personal loan?

A personal loan is an unsecured form of credit provided by banks and NBFCs for various individual financial needs, including medical expenses, home repairs, education, or travel. It does not require collateral, and repayment is made through fixed monthly instalments over a defined tenure, making it a flexible and widely accessible borrowing option.

Is a personal loan good or bad?

A personal loan can be beneficial when utilised for essential requirements, emergencies, or consolidating high-interest debt. However, it may become financially burdensome if borrowed without proper assessment of repayment capacity. Its suitability depends on the borrower’s financial discipline, income stability, and overall planning, making it neither inherently good nor bad.

How does a personal loan work?

A personal loan operates on a structured repayment schedule where the borrower receives a fixed sanctioned amount and repays it through Equated Monthly Instalments that include both principal and interest. Approval is based on factors such as credit score, income, and eligibility. Prompt repayment supports a strong credit profile and access to future credit.

What are the risks of a personal loan?

The risks associated with personal loans include relatively higher interest rates, penalty charges for delayed EMIs, and potential negative impact on the borrower’s credit score if payments are missed. Excessive personal loan borrowing may also lead to increased debt stress. Proper assessment of affordability and timely repayment remain essential to avoid these risks.